Introduction

When a customer finances a vehicle, the moment they drive off the lot, the car's value drops—sometimes by 20% or more in the first year alone. If the vehicle is totaled in an accident or stolen and not recovered, standard auto insurance pays only the car's current market value (its actual cash value, or ACV), not what the customer still owes on the loan.

This gap between the loan balance and the vehicle's depreciated value can leave borrowers owing thousands of dollars on a car they no longer have.

Guaranteed Asset Protection (GAP) insurance covers this financial shortfall. It bridges the difference between what the insurer pays and what the customer still owes the lender, protecting borrowers from owing money on a totaled or stolen vehicle.

According to Edmunds, new vehicles can lose 23.5% of their MSRP in the first year, and nearly 30% of trade-ins in Q4 2025 carried negative equity, with the average negative equity amount hitting an all-time high of $7,214. For auto dealers who finance vehicles, GAP represents both a customer protection tool and—when structured through a reinsurance program—a significant profit opportunity.

TLDR:

- GAP covers the gap between your loan balance and your car's actual cash value after a total loss

- Standard insurance pays only current market value, leaving you responsible for the remaining loan balance

- You can purchase GAP through insurers, dealers, or lenders—prices vary widely by channel

- GAP is most valuable during the first few years when depreciation outpaces loan payments

- You can cancel GAP once you have positive equity and may get a refund

How Does GAP Insurance Work?

The Depreciation Problem

Vehicle depreciation creates the fundamental problem GAP insurance solves. The moment a new car leaves the dealership, its market value begins declining rapidly.

Kelley Blue Book reports that new vehicles typically lose 20% or more of their value in the first year, with total depreciation reaching approximately 30% by year two and nearly 40% by year three. Meanwhile, your loan balance decreases much more slowly, especially in the early months when most of each payment goes toward interest rather than principal.

This timing mismatch creates negative equity—the period when you owe more than the car is worth. For buyers who financed with little or no down payment, negative equity exists from day one and can persist for years.

A Concrete Example

To see how this gap develops, here's how the numbers work in a real-world scenario:

- Original loan amount: $25,000

- Vehicle's actual cash value (ACV) after 18 months: $19,000

- Remaining loan balance: $22,000

- Standard insurance payout (minus $500 deductible): $18,500

- Your out-of-pocket responsibility without GAP: $3,500

- GAP insurance coverage: Pays the $3,500 difference

Without GAP coverage, you would owe $3,500 on a vehicle you no longer own, while still needing to finance a replacement vehicle.

The Claims Sequence

Understanding the example above, the actual claims process follows a specific sequence when your vehicle is declared a total loss or stolen and not recovered:

- Primary insurance pays ACV: Your comprehensive or collision coverage pays the vehicle's actual cash value, minus your deductible

- GAP calculates the difference: GAP coverage determines the gap between the ACV payout and your outstanding loan balance

- GAP pays the remaining balance: The GAP policy pays the difference directly to your lender (up to the policy's coverage limit)

Understanding Deductible Interaction

Most GAP policies do not cover your comprehensive or collision deductible. The deductible is subtracted from the actual cash value (ACV) before GAP calculates the covered amount.

For example, if your vehicle's ACV is $20,000 and your deductible is $500, your primary insurer pays $19,500. GAP then covers the difference between $19,500 and your loan balance—not between $20,000 and your loan balance.

Some GAP products offer a deductible waiver as an add-on feature, covering up to a specified amount (commonly $1,000).

Policy Payout Caps

Not all GAP policies provide unlimited coverage. Most policies cap payouts at 125% to 150% of the vehicle's ACV. For instance, Progressive's loan/lease payoff coverage caps at 125% of ACV—meaning if your vehicle is worth $20,000, the maximum total coverage ceiling is $25,000. If your outstanding loan balance exceeds that cap, you remain responsible for the difference.

These percentage-based caps matter most for borrowers who are significantly underwater on their loans, particularly those who rolled over negative equity from a previous vehicle.

What Does GAP Insurance Cover (and Not Cover)?

Covered Scenarios

GAP insurance applies in two specific situations:

Total Loss Events: Your insurer declares the vehicle a total loss after an accident, natural disaster, flood, fire, or other covered event. This happens when repair costs exceed the vehicle's actual cash value.

Theft Without Recovery: Thieves steal your vehicle and it remains unrecovered within your insurer's specified timeframe (typically 30 days).

In both scenarios, GAP covers the dollar gap between your insurer's ACV payout and your outstanding loan or lease balance. Nothing more, nothing less.

What GAP Does NOT Cover

GAP has clear boundaries. Understanding what it excludes prevents surprises when you file a claim:

- Mechanical repairs or engine failure: GAP is not a warranty

- Routine maintenance or wear-and-tear: Oil changes, brake pads, and similar costs are excluded

- Property damage to other vehicles: Liability coverage handles third-party damage

- Medical expenses: Personal injury protection or medical payments coverage applies instead

- Carry-over negative equity from a previous loan: Many policies exclude balances rolled over from prior vehicles

- Past-due loan payments: Delinquent payments and late fees are typically excluded

- Extended warranties or add-ons financed into the loan: Only the core vehicle loan balance is covered

- Your insurance deductible: Unless your policy includes a deductible waiver

The Overdue Payments Nuance

If you've fallen behind on your loan, many GAP policies will not cover the excess balance created by missed payments. According to the CFPB's Supervisory Highlights, GAP waivers typically cover the loan balance "minus any unpaid loan payments or similar charges" when the loss occurs. Any delinquent payments or late charges you accumulated before the loss won't be covered.

GAP Requires Primary Coverage

GAP cannot be purchased as standalone primary coverage. You must maintain active comprehensive and collision insurance on the vehicle for GAP to function. If you drop your primary coverage, your GAP coverage becomes void.

When Do You Need GAP Insurance?

Low Down Payment Scenarios

Buyers who put down less than 20% of the vehicle's purchase price start with immediate negative equity. Industry guidance from Kelley Blue Book recommends a 20% down payment as the minimum to avoid being underwater from day one. If you financed 90% or more of the purchase price, you're at high risk of owing more than the vehicle's worth for several years.

Long Loan Terms

Down payment size isn't the only factor—loan duration plays an equally important role in creating negative equity gaps.

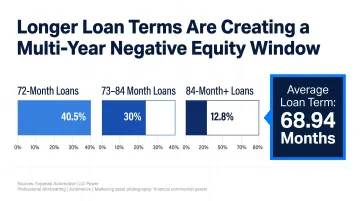

Longer financing terms extend the period of negative equity. According to Experian's Q4 2025 data, the average new car loan term is 68.94 months, with 69.08% of all new car loans extending 61 months or longer.

The trend toward extended terms has accelerated:

- 72-month loans now account for 40.5% of all auto sales

- 84-month+ loans have grown to 12.8% of sales (up from 7.3% in March 2019)

- Approximately 30% of new car loans stretch 73-84 months (up from 26.03% in Q4 2024)

With these extended terms, principal pays down slowly while the vehicle depreciates rapidly, creating a multi-year window of vulnerability.

Lease Requirements

Many leasing companies require GAP coverage because the lessee doesn't own the asset and remains responsible for the residual value gap. Edmunds notes that "most lease contracts automatically include GAP coverage," though consumers should verify terms and conditions. Leasing accounted for 24.37% of new vehicles in Q4 2025, making this a significant segment where GAP is standard.

Loan Rollovers

Buyers who rolled negative equity from a prior trade-in into a new loan start even further underwater. If you owed $5,000 more than your trade-in was worth and rolled that balance into your new $30,000 loan, you now owe $35,000 on a vehicle worth $30,000 before it even leaves the lot. This group especially needs GAP, though some policies exclude coverage for rolled-over balances—verify your policy's terms.

When GAP Is NOT Necessary

You can skip GAP coverage if:

- You made a down payment of 20% or more

- You're paying off the loan aggressively and will reach positive equity quickly

- Your loan balance is already below the vehicle's current ACV

- You have sufficient cash reserves to cover a potential gap

Once you reach positive equity, GAP provides no value and should be cancelled to stop paying premiums.

Where Can You Buy GAP Insurance?

Three Main Purchase Channels

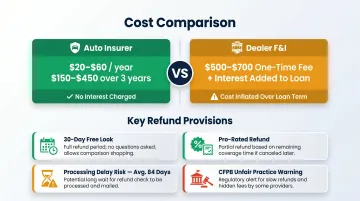

Auto Insurance Companies: Most major insurers offer GAP as an endorsement added to your existing comprehensive and collision policy. This is typically the most cost-effective option, with annual premiums ranging from $20-$60 depending on the insurer and your vehicle.

Dealerships (F&I Products): Dealers offer GAP at the point of sale, often rolled into your loan as a one-time charge. Dealer GAP typically costs $500-$700, though some charge as much as $900. Because this amount is financed, you'll pay interest on the GAP premium for the life of the loan.

Lenders or Banks: Some financial institutions offer GAP at loan origination, either as a separate product or bundled into loan terms.

Cost Implications: Insurer vs. Dealer

Buying through your auto insurer is significantly cheaper than financing GAP through a dealer. Over three years, insurer-provided GAP costs $150-$450 total, compared to $500-$700+ from a dealer. More importantly, when you finance dealer GAP into your loan, you pay interest on that premium. The CFPB warns that "if you choose to finance a GAP policy into your loan, it will add to your total loan amount, which ultimately increases what you'll pay in total interest over time."

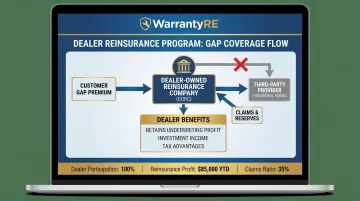

The Dealer's Perspective: Reinsurance Programs

For auto dealers, GAP represents a significant profit opportunity when structured properly. Dealers who offer GAP as a finance-and-insurance (F&I) product can generate substantial revenue from the spread between what they charge customers and what they pay to the GAP provider.

When dealers partner with a reinsurance program—such as WarrantyRE—they can capture that profit themselves rather than passing it to a third-party insurer.

WarrantyRE has helped over 400 auto dealers establish reinsurance programs that include GAP coverage. Through this structure, dealers create their own reinsurance company to administer GAP policies.

Key advantages include:

- Premiums flow into the dealer-owned reinsurance company instead of a third-party provider

- Dealers retain all underwriting profits

- A dealer selling 150 GAP policies annually at $499 each generates $75,000 in receivables

- Revenue stays in-house rather than going to an external vendor

This approach works for franchise, retail, and Buy Here Pay Here dealerships. WarrantyRE handles all claims administration, compliance filings, and performance reporting, ensuring dealers maintain regulatory compliance while maximizing profitability.

The reinsurance structure includes:

- A-rated insurer backing

- 150% or 125% loan-to-value coverage caps

- Deductible coverage up to $1,000

How Much Does GAP Insurance Cost?

Main Cost Variables

GAP pricing depends on several factors:

Purchase Channel:

- Auto insurer endorsement: $20-$60 per year

- Dealer F&I product: $500-$700 one-time (often financed)

Vehicle Type: Luxury and high-performance vehicles typically cost more to insure, which increases GAP premiums proportionally.

Loan Amount and Term: Larger loans and longer terms increase risk, which can raise premiums.

Coverage Limits: Policies with higher percentage caps (150% vs. 125% of ACV) may cost more.

Duration Considerations

GAP coverage is only needed while your loan balance exceeds the vehicle's ACV—typically the first 2-4 years of a loan. Buyers should monitor their loan-to-value ratio and cancel coverage once they reach positive equity.

Continuing to pay for GAP after reaching positive equity wastes money on protection you no longer need.

Pro-Rated Refund Rights

When GAP coverage ends early, consumers can often recover unused premiums. Understanding your refund rights protects you from paying for coverage you no longer need.

The CFPB confirms that if you sell, refinance, or prepay your auto loan, you can receive a pro-rated refund on unused GAP coverage.

Key refund provisions include:

- 30-day "free look" period: Some states require full refunds if you cancel within 30 days

- Pro-rated refunds: State laws often require refunds when financing contracts or leases end early

- Processing delays: The CFPB's Supervisory Highlights found servicers delayed refunds an average of 84 days, with some delays reaching 423-664 days

- Unfair practices: The CFPB has declared it unfair for servicers to fail to request and apply refunds promptly

GAP Insurance vs. GAP Waiver: What's the Difference?

Legal Distinction

GAP Waiver (Debt Cancellation Agreement):

- Contractual agreement where the lender agrees to "waive" or forgive the remaining loan balance above the vehicle's ACV in a total loss

- Not technically insurance and regulated differently in most states

- Dealer or lender typically purchases backing insurance (CLIP or RIP) to protect from financial risk

GAP Insurance:

- Policy between an insurance company and the insured customer

- Insurance company handles payouts; dealer acts as licensed selling agent

- Subject to state insurance regulations and licensing requirements

Practical Implications for Consumers

Both products cover the gap between ACV and loan balance, but their structure affects how dealers sell and administer them. A GAP waiver embeds into the loan agreement, while GAP insurance exists as a separate policy.

According to industry analysis, dealers sell GAP as a waiver in all but four states. In those four states, it's structured as insurance, determined by each state's Department of Insurance.

For dealers, this distinction matters because regulatory protections and cancellation rights differ between the two structures. Some states have specific disclosure requirements and refund provisions that apply to one type but not the other, affecting how you present the product to customers.

Frequently Asked Questions

What does gap insurance actually pay for?

GAP insurance pays the difference between your outstanding loan balance and your vehicle's actual cash value after a total loss. Your comprehensive or collision deductible is subtracted before GAP coverage kicks in.

Do I have to pay the deductible if I have gap insurance?

Yes, in most cases. Your deductible is subtracted before GAP calculates coverage, unless your policy includes a deductible waiver (typically up to $1,000).

Can you buy gap insurance on its own?

No. GAP requires underlying comprehensive and collision coverage. While it can be purchased through dealers or lenders, you must maintain primary auto insurance for GAP to be valid.

What does dealer gap insurance cover?

Dealer GAP covers the same loan-to-value gap as insurer GAP. However, it's typically financed into your loan at $500-$700 versus $20-$60/year from insurers, meaning you pay interest on the premium.

Should I get guaranteed asset protection insurance?

GAP makes sense if you made a small down payment (under 20%), have a 60+ month loan, are leasing, or rolled over negative equity. Cancel it once your loan balance drops below the vehicle's market value.

What is 150 gap insurance?

"150% GAP" covers loan balances up to 150% of your vehicle's actual cash value, providing a higher safety margin for buyers significantly upside down on loans. Common alternatives include 125% GAP policies with lower coverage ceilings.