Introduction

The average vehicle on U.S. roads is now 12.8 years old, according to S&P Global Mobility's 2025 data. Most factory warranties expire long before that milestone.

When major repairs strike, the costs are staggering. The national average for all vehicle repairs sits at $838, but a single transmission replacement can run $5,892 to $6,402. For the 37% of Americans who couldn't cover a $400 emergency expense with cash, according to the Federal Reserve's 2025 report, these bills represent a serious financial threat.

Vehicle service contracts (VSCs), commonly called "extended warranties," exist to bridge this gap. But confusion runs deep: What exactly are they? How do they differ from factory warranties? Are they worth the cost?

This guide delivers clear answers on coverage, costs, and whether a VSC makes sense for your situation.

TLDR: Key Takeaways

- VSCs are paid service agreements covering mechanical repairs—not warranties under federal law

- Coverage source, scope, and timing differ from manufacturer warranties

- Costs vary from hundreds to thousands based on vehicle age and coverage tier

- One major claim can recover the full VSC cost on older, high-mileage vehicles

- Dealers using reinsurance models capture 100% of VSC profits instead of losing them to third-party providers

What Is a Vehicle Service Contract?

A vehicle service contract (VSC) is an optional, paid agreement between a vehicle owner and a provider that requires the provider to pay for certain covered repairs.

The Federal Trade Commission clarifies that a VSC is not technically a warranty because you purchase it separately—it's a service agreement, not part of the original sale.

You pay a premium (upfront or in installments), and when a covered mechanical failure occurs, you file a claim, pay any applicable deductible, and the VSC provider covers the repair cost at an authorized facility.

Who Sells Vehicle Service Contracts?

Three main sources sell VSCs:

- Automakers offer factory-backed extended warranties

- Dealerships sell VSCs, often administered by third-party companies

- Independent companies market VSCs directly to consumers

When evaluating VSC options, understanding who actually honors the contract matters.

Many dealership VSCs are handled by independent administrators who authorize and pay claims. If the dealer closes, the administrator may still fulfill the contract—and vice versa.

Key point: Always verify the obligor (the party legally responsible for paying claims) before signing.

Vehicle Service Contract vs. Extended Warranty vs. Manufacturer's Warranty

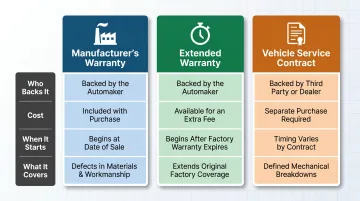

Manufacturer's Warranty

Every new vehicle includes a manufacturer's warranty at no extra cost. It covers defects in materials and workmanship for a defined period—typically 3 years/36,000 miles bumper-to-bumper and 5 years/60,000 miles for the powertrain. This is a legal promise from the automaker.

Extended Warranty

Technically, a true extended warranty only comes from the original manufacturer and extends the factory warranty's duration or scope. However, many companies use "extended warranty" to describe what is legally a VSC.

The FTC warns that scammers exploit this terminology with urgent-sounding mailers claiming your "warranty is expiring."

Key Differences

Understanding how these three warranty types compare helps clarify which coverage applies when.

| Factor | Manufacturer's Warranty | Extended Warranty (Factory) | Vehicle Service Contract |

|---|---|---|---|

| Backed by | Automaker | Automaker | Third party, dealer, or independent company |

| Cost | Included with purchase | Extra fee | Separate purchase |

| Coverage start | Immediately at purchase | After factory warranty expires | Varies; can overlap with factory warranty |

| What's covered | Defects in materials/workmanship | Extends factory coverage | Defined list of mechanical breakdowns |

Common misconceptions about VSC timing:

- Myth: VSCs always begin after factory warranties expire

- Reality: Some VSCs start while factory coverage is active

- Benefit: Fills gaps the manufacturer warranty doesn't address—such as wear-and-tear items or specific components

What Does a Vehicle Service Contract Cover — and What It Doesn't

Coverage Tiers

VSCs typically offer three levels:

Powertrain Coverage

- Engine internals, transmission, drive axle

- Most affordable but narrowest protection

- Best for newer vehicles with reliable histories

Mid-Tier (Stated Component)

- Powertrain plus electrical, A/C, suspension, steering

- Covers only specifically listed components

- More affordable but higher claim denial risk

Comprehensive (Exclusionary)

- Covers everything except a stated exclusion list

- Often called "bumper-to-bumper" coverage

- Most expensive but broadest protection and lowest denial risk, providing superior protection since only listed items are excluded rather than only listed items being included

Understanding tier options helps you evaluate which components matter most for your situation.

Commonly Covered Components

- Engine internals (pistons, crankshaft, valves)

- Transmission (gears, torque converter)

- A/C compressor (average replacement: $1,004-$1,356)

- Fuel system (injectors, pump—$1,125-$1,247 to replace)

- Electrical (alternator $757-$1,032, starter $744-$837)

- Steering and suspension

- Cooling system

- High-tech components (infotainment, sensors)

What's NOT Covered

- Pre-existing conditions

- Normal wear and tear (brake pads, tires, wiper blades)

- Cosmetic damage

- Accident or neglect damage

- Issues from skipped maintenance (missed oil changes can void coverage)

Add-On Benefits

Many VSCs bundle extras:

- 24/7 roadside assistance (towing, lockout, battery jump)

- Rental car reimbursement during covered repairs

- Trip interruption coverage

Read the Fine Print

Two plans with similar marketing can differ dramatically. Check:

- Deductible structure (per visit vs. per repair)

- Whether the plan covers labor rates fully

- Whether the plan uses remanufactured or new parts

- Pre-authorization requirements

How Much Does a Vehicle Service Contract Cost?

VSC prices vary widely based on:

- Vehicle age and mileage

- Make and model (luxury vehicles cost more)

- Coverage level selected

- Contract duration

- Provider

These factors directly impact what you'll actually pay.

According to MarketWatch's 2024 analysis, monthly costs range from $100 to $150.

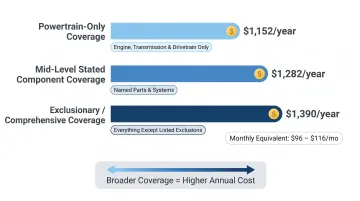

Annual pricing breaks down by coverage tier:

- Exclusionary plans: $1,390/year average

- Mid-level plans: $1,282/year average

- Powertrain-only: $1,152/year average

Payment Options

- Lump sum: Pay upfront, no interest

- Financed: Roll into car loan (but you'll pay interest on the VSC cost)

- Monthly: Flexible but potentially more expensive over time

Deductibles

Expect $0 to $200 per repair visit. Lower deductibles mean higher premiums. Factor this in when comparing plans.

Are Vehicle Service Contracts Worth It?

Whether a VSC makes financial sense depends on your specific situation. They deliver the most value for:

- Owners of older or high-mileage vehicles beyond factory warranty

- Drivers without significant emergency savings

- Owners of vehicles with known reliability issues

If you drive a newer vehicle still under factory warranty or maintain strong emergency savings, a VSC may offer limited immediate value.

When VSCs Deliver Clear Value

Used car buyers benefit most. Factory warranties have typically expired, and older vehicles face higher failure risk.

A single major repair can exceed the multi-year cost of a VSC:

- Transmission replacement: $5,892-$6,402

- Engine rebuild: $2,000-$10,000

The Honest Flip Side

Consumer Reports' 2025 survey revealed concerning statistics:

- 55% of extended warranty purchasers never used it

- Median price paid: $1,214

- Median benefit received: $837

- Average net loss: $377

These losses can be partially offset. Transferable VSCs can increase resale value by approximately $500 to $1,500, and refundable contracts may allow pro-rated cancellation if you sell the vehicle.

How to Choose the Right Vehicle Service Contract Provider

Key Vetting Criteria

Verify Financial Backing

- Who is the obligor (the party paying claims)?

- Is the obligor backed by an A-rated insurer?

- Check the provider's financial stability

Check Complaint History

- Review Better Business Bureau records

- Search state attorney general complaints

- Look for patterns of denied claims

Confirm Repair Network

- Can you use any licensed mechanic?

- Are you restricted to specific shops?

- What's the authorization process?

Avoid Common Scams

The FTC has documented widespread VSC fraud. Warning signs:

- Unsolicited calls, texts, or mailers claiming your "warranty is expiring"

- Pressure to provide financial information immediately

- Requests for deposits before receiving a written contract

Recent Enforcement Actions

In 2023, the FTC obtained $6.6 million in judgments against American Vehicle Protection for extended warranty scams.

In 2025, they sent $9.6 million in refunds to 168,179 consumers harmed by deceptive CarShield advertising.

For Auto Dealers: The Reinsurance Opportunity

Understanding VSC provider quality matters for dealers, too—especially those considering offering their own programs. Dealers who administer VSCs through a reinsurance structure capture 100% of underwriting profits that would otherwise go to third-party providers.

WarrantyRE has helped over 400 auto dealers build and manage their own reinsurance programs. This model allows dealers to:

- Control the claims experience and drive service work to their own facilities

- Retain all underwriting profits and investment income

- Improve customer satisfaction through faster, more personalized claims handling

- Benefit from tax-advantaged wealth creation

Rather than earning only a commission on VSC sales, dealers become their own warranty company. This keeps all service contract revenue within their business ecosystem.

Frequently Asked Questions

What is the difference between a warranty and a vehicle service contract?

A manufacturer's warranty comes with your vehicle and covers defects in materials and workmanship. A VSC is a separately purchased agreement covering mechanical breakdowns, often beyond factory warranty coverage.

What is covered by a vehicle service contract?

Coverage depends on plan tier. Most VSCs cover engine, transmission, A/C, electrical, and steering/suspension systems, but exclude wear-and-tear items, cosmetic damage, and pre-existing conditions.

How much does a vehicle service contract cost?

Costs vary by vehicle age, mileage, and coverage level. Expect $100-$150 monthly or $1,152-$1,390 annually, plus $0-$200 deductibles per repair.

Are vehicle service contracts worth it?

VSCs offer the most value for owners of older or high-mileage vehicles outside factory warranty coverage, particularly those who want protection against large, unexpected repair bills. Newer car owners still under warranty may find less immediate need.

Should I buy a vehicle service contract for a used car?

Used car buyers are often the best candidates for a VSC because factory warranties have typically expired, and older vehicles face a higher probability of mechanical failures. A VSC provides practical protection against costly surprises.

How do I choose the best vehicle service contract provider?

Verify the obligor's financial backing and check BBB reviews or state complaint records. Confirm repair network flexibility and read the full contract, including exclusions and deductibles, before signing.