This guide will walk you through what claims management is, how the process works from intake through resolution, the types of claims your business will encounter, why controlling this process matters financially, and how businesses can improve their approach — including how to capture the profits that currently flow to third parties.

TLDR

- Manage the full claim lifecycle from filing through resolution to control costs and customer satisfaction

- Service contracts, warranties, and liability claims directly impact your profitability and customer trust

- Third-party administrators control claims by default, costing you profits and consistent customer experiences

- Reduce costs, prevent fraud, and generate actionable data through effective claims management

- Own your warranty administration through reinsurance to capture premium surplus as profit

What Is Claims Management?

Claims management is the structured, end-to-end process used to receive, investigate, evaluate, and resolve claims arising from insurance policies, service contracts, or warranty programs.

It applies across industries — from insurance carriers to home service contractors to auto dealers — wherever a customer seeks coverage for a loss or repair.

Claims management vs. claims processing: Processing handles transactional tasks like submitting paperwork and cutting checks. Management takes a strategic approach — overseeing the full lifecycle, controlling outcomes, and using data to improve future performance.

In the warranty context: When a customer experiences a covered system or product failure and calls for repair, that triggers a warranty claim. The administrator — whether a third-party provider or the contractor's own company — manages that claim through review and resolution.

The US home warranty market reached $4.6 billion in 2025, while auto extended warranties hit $32.7 billion, demonstrating the massive scale of warranty claims nationwide.

Who Manages Claims

Four types of entities manage claims:

- Insurers: Traditional insurance companies managing their own policyholder claims

- Third-party administrators (TPAs): Independent firms hired to process claims on behalf of others

- Self-insured businesses: Companies that handle their own claims directly without external administrators

- Administrator-obligor reinsurance companies: Businesses that establish their own warranty companies (like those WarrantyRE helps clients create), administering claims while capturing underwriting profits

The choice of who manages your claims determines your level of control and profit retention.

Having the right people, processes, and documentation in place separates efficient claims management from reactive, costly claims handling — whether you're a large insurer or a regional HVAC company.

The Claims Management Process: Step by Step

Step 1: Claim Intake and First Notice of Loss

The process begins when a claimant (customer, policyholder, or service contract holder) reports an incident or requests service under their coverage. Critical information captured at intake includes:

- Nature of the issue and date of occurrence

- Contract or policy details and coverage scope

- Relevant supporting documentation (photos, receipts, prior service records)

- Contact information and preferred resolution timeline

Thorough intake prevents downstream delays and disputes. Missing documentation creates costly problems that surface during investigation and settlement.

Step 2: Investigation and Verification

During investigation, the claims team verifies that the claim falls within the scope of the contract or policy. Key activities include:

- Coverage verification: Confirming the claim is covered under the terms of the agreement

- Validity assessment: Determining whether the claim is legitimate or potentially fraudulent

- Evidence gathering: Collecting inspection reports, photos, technician diagnoses, and service records

Fraudulent or invalid claims are caught early in this phase.

Research shows that claims reported within 3 days cost 48% less than those reported after 29+ days. Prompt, thorough investigation directly controls costs and prevents overpayments.

Step 3: Evaluation and Adjudication

Once investigation is complete, adjudication determines whether the claim is valid, what amount or scope of repair is covered, and the total liability.

A claims adjuster or administrator applies policy terms fairly and consistently, balancing customer satisfaction with financial responsibility.

Cost outcomes and reserve accuracy hinge on this step. Inconsistent decisions lead to overpayments, customer disputes, and eroded profit margins.

Step 4: Settlement and Resolution

After evaluation, resolution involves approving or denying the claim, issuing payment to repair networks or service technicians, or communicating a denial with clear reasoning.

Speed and transparency drive customer satisfaction at this stage.

According to J.D. Power's 2026 U.S. Property Claims Satisfaction Study, the average repair cycle time dropped to 29.6 days. Faster cycle times drove overall satisfaction up 20 points to 702 out of 1,000.

Customers using insurer-approved contractor networks saw high-severity claims complete more than 2 weeks sooner than those not using such networks.

Step 5: Documentation, Reporting, and Closeout

Every action taken during the life of a claim must be recorded: notes, reserve changes, communications, and settlement amounts. Data compiles into reports that reveal patterns such as:

- Recurring failure types

- High-cost claim categories

- Fraud indicators

- Technician performance trends

Documentation becomes the foundation for continuous improvement.

Businesses that analyze claims data can identify installation errors, product quality issues, and training gaps. Warranty programs that capture and act on this intelligence turn claims management from a cost center into a profit-driving advantage.

Types of Claims

Warranty and Service Contract Claims

These are the most relevant claims for home service contractors and auto dealers. They arise when covered equipment, systems, or vehicles fail and the customer calls for repair or replacement under their plan.

Common contractor claims:

- Refrigerant leaks, bad contactors, and labor-related installation issues (HVAC)

- Leaks, flashing issues, and improper nail patterns (Roofing)

- Leaks under sinks, failed fittings, and improperly seated water heaters (Plumbing)

- Service work callbacks and labor warranty issues (Electrical)

Common dealer claims:

- Mechanical breakdowns in covered components (Vehicle Service Contracts)

- Coverage when a vehicle is totaled and loan exceeds value (GAP)

- Physical damage coverage when customers lack required insurance (Collateral Protection Insurance)

Coverage scope—labor, parts, consequential damage—determines administrator payout responsibility.

Other Common Claim Types

Beyond warranty claims, contractors and dealers may encounter:

- Property damage claims: Arising from work performed on a customer's home

- Liability claims: When a service technician causes accidental damage or injury

- Product defect claims: Manufacturer or installer liability

Each type follows the same general process but requires different documentation.

Simple warranty claims on a single component are straightforward to process. Liability or consequential damage claims may require legal review and higher reserve amounts.

Why Claims Management Matters for Your Business

The Financial Stakes

Every unresolved, mismanaged, or fraudulent claim hits profit margins directly. Paid losses combined with investigative and settlement expenses accounted for approximately 70% of US premiums collected in 2020, establishing claims as the single largest cost category.

Poor claims experiences put up to $170 billion of global insurance premiums at risk over a five-year period through 2027, according to Accenture research. If your third-party warranty provider is settling claims generously or inefficiently, those costs are built into your premiums or program fees.

The Customer Experience Impact

A slow, confusing, or denied claim is often the last interaction a customer has with a business before deciding not to renew or refer. Satisfied insurance customers are 80% more likely to renew their policies than unsatisfied customers, and US auto insurance carriers providing best-in-class customer experiences generated 2 to 4 times more new-business growth.

31% of home and auto insurance claimants were not fully satisfied with their claims-handling experience. Of dissatisfied claimants, 30% had already switched carriers, and 47% were considering switching. Claims management is a brand moment — how you handle a broken HVAC unit or failed transmission says everything about your company.

The Hidden Cost of Giving Away Claims Control

Understanding the financial impact of claims is one thing. Controlling who profits from them is another.

The premiums paid to third-party warranty providers include a built-in margin for claims profit. When claims cost less than premiums collected, the third party keeps that surplus.

Business owners who understand this dynamic see why owning their claims administration is a strategic profit lever.

One approach to reclaiming this control is the administrator-obligor reinsurance structure, where contractors and dealers establish their own warranty companies. In structures like WarrantyRE's program, claims are fully managed from the first customer call to final resolution.

The key difference: approved claims are paid from a reinsurance account owned by the business, and unused funds remain as profit for the business owner — not a third party.

By establishing their own reinsurance company, businesses gain:

- Direct control over claims approval and customer service standards

- Retained premium surplus as profit rather than third-party margin

- A customer experience that reflects their brand, not an outsourced provider's policies

Key Challenges in Claims Management

Fraud and Bad-Faith Claims

Fraudulent claims represent a significant source of loss across the industry. Insurance fraud costs the US $308.6 billion annually across all lines, with $45 billion attributed to property and casualty insurance specifically.

Common fraud patterns include customers claiming damage that isn't covered, service technicians padding invoices, or staged incidents.

Verification procedures, documentation requirements, and pattern recognition are essential for catching fraud before settlement. WarrantyRE's full-service claims administration includes verification protocols designed to ensure claim legitimacy while maintaining efficient processing.

Delayed Reporting and Incomplete Documentation

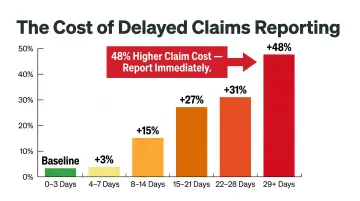

Claims reported late or without sufficient supporting detail are harder to investigate, more expensive to resolve, and more likely to result in disputes. Liberty Mutual's research shows that claims reported after 29+ days cost 48% more than those reported within 0-3 days.

The cost escalation by delay period:

- 4-7 days: 3% increase

- 8-14 days: 15% increase

- 15-21 days: 27% increase

- 22-28 days: 31% increase

- 29+ days: 48% increase

These escalating costs make proper documentation critical from day one. Clear intake protocols that capture complete information at first contact prevent costly delays and disputes down the line.

WarrantyRE provides structured intake and documentation standards to minimize delays and ensure complete information from the start.

Regulatory Compliance and Jurisdictional Complexity

Warranty and service contract programs are regulated differently by state, and claims handling must comply with applicable laws governing coverage disclosures, denial procedures, and payment timelines.

The NAIC Service Contracts Model Act provides a regulatory framework, but adoption varies significantly by state. Many states require service contract providers to:

- Register with the Department of Insurance

- Obtain licenses and maintain funded reserves or reinsurance backing

- Comply with specific disclosure obligations

WarrantyRE manages all legal forms, filings, tax returns, and renewals for clients' reinsurance companies, ensuring compliance with IRS Code 831(b) and state licensing requirements.

The company operates nationwide, handling multi-state compliance so clients can offer warranty programs confidently across jurisdictions.

How to Improve Your Claims Management Process

Establish Structured Intake and Documentation Standards

Strengthen your claims process from day one with:

- Standardized intake forms capturing all required information

- Required photo documentation at time of claim

- Clear technician reporting protocols

- Defined timelines for each stage of the process

Consistent documentation is the foundation for both compliance and fraud prevention.

For businesses establishing or improving their intake standards, WarrantyRE provides comprehensive onboarding and training programs covering claims intake, documentation protocols, and technician reporting.

Use Claims Data to Reduce Future Losses

Businesses with strong claims management don't just resolve individual claims — they analyze the aggregate data. Recurring failure types may point to installation errors, product quality issues, or training gaps.

Data-driven claims management delivers measurable results. According to McKinsey research, establishing analytics-driven feedback loops can trigger a 5-percentage-point improvement in combined ratios within 12 months.

Key analytics capabilities to implement:

- Tracking recurring failure patterns by product, installer, or timeframe

- Monitoring claim resolution times and bottlenecks

- Identifying seasonal or regional trends

- Measuring the financial impact of specific claim types

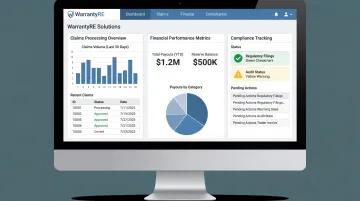

WarrantyRE's performance reporting and claims analytics provide clients with detailed insights including claims processing details, financial performance metrics, and compliance tracking — enabling businesses to identify trends, maximize profits, and make informed decisions.

Work with an Experienced Claims Administrator Who Aligns with Your Business Goals

Many contractors and dealers don't have the in-house resources to manage claims at scale. Choosing the right administrative partner determines whether your warranty program becomes a profit center or an operational burden.

WarrantyRE's full-service administration includes:

- Full claims management from first customer call to final resolution

- Compliance handling for all legal forms, filings, tax returns, and renewals

- Performance analytics revealing trends, costs, and improvement opportunities

- Financial oversight including monthly statements, annual reports, and investment management

This gives home service businesses and auto dealers the infrastructure of a professional warranty company without the complexity of building it from scratch. Clients who have transitioned to WarrantyRE's model report capturing underwriting profits, reducing out-of-pocket warranty expenses, and improving customer satisfaction through seamless claims administration.

Frequently Asked Questions

What is claims management in insurance?

Claims management is the process administrators use to handle coverage requests from initial filing through investigation, adjudication, and settlement. It includes operational execution and strategic oversight across the entire claims lifecycle.

What is a claims management system?

A claims management system combines software, processes, and workflows to track, evaluate, and resolve claims efficiently. It typically includes intake forms, documentation storage, reporting dashboards, and financial tracking.

Are claims management companies legitimate?

Legitimate claims administrators are regulated, transparent, and focused on fair resolution. Vet administrators by checking compliance credentials, fee structures, performance history, and backing by A-rated insurers.

Is it worth using a claims management company?

Professional claims administration reduces errors, improves customer experience, and ensures compliance. Contractors and dealers should also evaluate whether owning their claims administration through reinsurance—like WarrantyRE offers—captures more profit than third-party models.

What are the 4 types of claims?

The four common types are property (physical asset damage), liability (legal responsibility for injury), warranty/service contract (repair or replacement coverage), and health/life (medical payouts). Contractors and dealers primarily handle warranty and liability claims.

What does an insurance claims manager do and what skills are required?

A claims manager oversees the full claims lifecycle—assigning adjusters, reviewing reserves, ensuring compliance, and analyzing performance. Key skills include regulatory knowledge, attention to detail, communication, and balancing customer satisfaction with financial responsibility.