Introduction

The warranty program you choose for your HVAC business determines who profits from your customer relationships. Most contractors default to third-party providers without realizing the financial impact.

Here's what happens when you sell third-party extended warranties:

- The provider collects all premiums and manages claims

- You receive a 24-30% sales commission

- The provider keeps 70-76% of the revenue—including all underwriting profit

- You lose control of the customer warranty experience

This creates a fundamental question: should you hand warranty profits to outside companies, or capture that revenue yourself?

This guide covers the types of warranty programs available to HVAC contractors, the key factors to evaluate when choosing one, and why some businesses are moving toward owning their warranty structure entirely through reinsurance-backed programs.

TLDR

- Four warranty options: manufacturer warranties, third-party providers, self-funded plans, or reinsurance-backed programs

- Third-party providers retain 70-76% of warranty premiums as underwriting profit and investment income

- Reinsurance-backed warranty companies let contractors capture 100% of customer-generated profits

- Key selection factors: coverage scope, claims control, profit retention, and financial backing

- Reinsurance models turn each installation into recurring revenue while reducing callback costs

What Is an HVAC Warranty Program?

An HVAC warranty program is a service agreement offered at installation, promising repair or replacement coverage for system failures within a specified period. For contractors, these programs fill gaps left by manufacturer warranties while creating ongoing customer relationships.

Three Distinct Components

Manufacturer warranties cover equipment defects. Major brands like Carrier, Trane, and Lennox typically provide 5-10 years of parts coverage (10 years if registered within 60-90 days, 5 years if not). Heat exchangers often carry 20-year to lifetime warranties.

However, no manufacturer includes labor in their standard warranty—this is the primary gap contractors must address.

Labor warranties cover installation workmanship. The installing contractor provides these and assumes the liability for installation quality.

When callbacks occur due to installation issues—refrigerant leaks from faulty connections, bad contactors, or improper ductwork—the labor warranty covers the correction costs.

Extended service contracts are sold separately for an additional fee. Under the FTC's Magnuson-Moss Warranty Act (16 CFR 700.11), these are legally distinct from written warranties because they require separate payment and may be entered into after the sale.

Extended contracts typically cover both parts and labor beyond the manufacturer warranty period, creating a recurring revenue opportunity for contractors.

Types of HVAC Warranty Programs for Contractors

Manufacturer Warranties

These come standard with HVAC equipment from brands like Carrier, Trane, Lennox, Goodman, and Rheem. They protect homeowners from equipment defects but offer contractors minimal financial benefit or claims control.

Coverage duration:

- Unregistered parts: 5 years (all major brands)

- Registered parts: 10 years (requires registration within 60-90 days)

- Compressor: 10 years registered (Carrier, Trane, Lennox) to lifetime (select Goodman models)

- Heat exchanger: 20 years to limited lifetime

- Labor: Not included by any manufacturer

The registration window matters. Contractors who fail to register systems within 60-90 days leave their customers with half the parts coverage. But even with registration, labor costs remain the contractor's responsibility.

Third-Party Extended Warranty Providers

These external companies administer service contracts sold by contractors to customers. Providers like JB Warranties, Trinity Warranty, and NAHG/ServiceGuard handle compliance, claims, and financial backing.

The contractor collects premiums at point of sale and remits them to the provider, retaining a sales margin.

Revenue sharing reality: According to industry data, contractors selling third-party extended warranties earn margins of 24-30%. The provider retains all underwriting profit and investment income beyond that commission.

Warranty Week analysis shows the extended warranty sector targets a 65% loss ratio with a 25% expense ratio for a 10% underwriting profit. This means 10% of every premium dollar becomes pure profit for the administrator, not the contractor.

Advantages:

- No administrative burden

- No compliance responsibility

- No claims risk

Disadvantages:

- Limited profit retention

- No claims control

- No customer data ownership

- No recurring revenue beyond commissions

Contractor-Branded Service Plans

Some HVAC businesses create their own maintenance plans or service agreements funded from operating cash. These build recurring revenue and customer loyalty.

Industry data shows contractors with active service agreements report 20-40% higher annual revenue per customer. Plus, 78% of agreement customers purchase equipment replacements from their existing provider.

Financial risk: The contractor bears full liability for future claims without reinsurance backing. If major repair costs arise (compressor failure, heat exchanger crack, or refrigerant leak), the contractor absorbs claims directly.

Many states also require registration and financial assurance (reserve accounts, surety bonds, or minimum net worth thresholds) even for contractor-administered programs.

Reinsurance-Backed Warranty Programs

For contractors seeking control without bearing full financial risk, reinsurance-backed programs offer a middle path. This model allows contractors to establish their own administrator obligor company, supported by A-rated insurers.

Customer premiums flow into the contractor's own entity rather than a third-party provider. The reinsurance carrier provides claims backstop, while the contractor captures 100% of underwriting profit and investment income.

How it works:

- Contractor incorporates a warranty company (the obligor)

- Warranty fees are built into job pricing and deposited into the reinsurance account

- A-rated reinsurer provides financial backing and regulatory compliance

- Contractor controls claims approval and customer experience

- Unused warranty funds remain with the contractor as profit

- Investment income on premium reserves belongs to the contractor

This structure transforms warranty liability into a controlled revenue stream while meeting state regulatory requirements for financial assurance.

Key Factors to Consider When Choosing a Warranty Program for Your HVAC Business

Selecting the right warranty program is not just a customer service decision—it's a profitability and risk management decision. The program you choose affects revenue predictability, claims costs, and brand reputation.

Coverage Scope and Flexibility

Coverage terms determine customer satisfaction and claim disputes. A warranty that excludes common failure points generates complaints that damage your brand.

Common HVAC failures and their typical repair costs include:

- Capacitor replacement: $150-$350

- Refrigerant recharge (R-410A): $250-$600

- Blower motor replacement: $400-$900

- Control board replacement: $350-$900

- Heat exchanger repair/replacement: $500-$2,500+

- Compressor replacement: $1,500-$3,000+

Programs with rigid third-party terms may exclude refrigerant leaks, pre-existing conditions, or lack of maintenance documentation. Contractors should look for programs allowing them to set or influence coverage terms rather than defaulting to templates that may not align with what they've promised customers at point of sale.

Here's the risk: If your sales team promises comprehensive coverage but your third-party provider denies claims based on fine print, you lose the customer relationship—and the referrals that follow.

Claims Control and Process

When a third party handles claims, you lose visibility into repair decisions, technician selection, and turnaround time. All of these directly impact customer satisfaction and repeat business.

Why this matters to your bottom line:

- Third-party administrators may authorize repairs through the lowest bidder, not your service team

- Slow claim approvals frustrate customers who associate delays with your brand

- Over-authorized repairs inflate loss ratios and threaten program sustainability

- You have no data on claim frequency, root causes, or technician performance

Programs where the contractor controls claims processing protect profit margins by preventing unnecessary authorizations and preserve the customer relationship by ensuring faster, quality-controlled service.

Profit Retention vs. Revenue Sharing

Third-party warranty providers earn their margin by collecting premiums and paying out only a portion in claims. The profit differential stays with them.

The extended warranty sector operates on well-documented benchmarks. According to Warranty Week, typical economics include:

- Target loss ratio: 65% (claims paid as percentage of premiums)

- Typical expense ratio: 25%

- Target underwriting profit: 10%

- Retail markup: At least 50% of contract price covers costs unrelated to risk

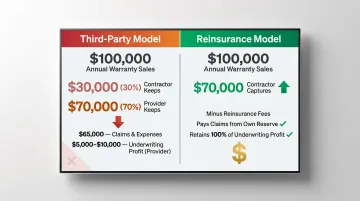

Here's how this affects your business: If you sell $100,000 in third-party warranties annually and retain a 30% margin, you keep $30,000. The provider collects $70,000.

The provider pays approximately $65,000 in claims and expenses, then retains $5,000-$10,000 in underwriting profit—plus all investment income on reserves.

Under a reinsurance-backed model, you capture that entire $70,000 (minus reinsurance premiums and administration fees), pay claims from your reserve pool, and retain 100% of underwriting profit and investment income.

Administrative Burden and Support

Some warranty structures require contractors to handle compliance, bookkeeping, tax filings, claims processing, and customer communications. This overhead can negate profitability if not managed correctly.

State regulations add complexity. The NAIC's Spring 2023 chart documents that the majority of U.S. states regulate service contracts, with most requiring one of three financial assurance methods:

- Reimbursement insurance policy (CLIP) from an authorized insurer

- Funded reserve account (often 40% of gross consideration) plus security deposit (often 5%, minimum $25,000)

- Minimum net worth of $100 million

Contractors selling third-party programs rely on the provider for compliance. Contractors operating self-funded plans or reinsurance models must either register in every operating state or partner with an administrator that handles multi-state filings, renewals, and reporting.

The best programs offer full-service administration covering legal forms, state filings, reporting, financials, and claims handling. This lets you focus on installations and service calls.

Provider Credibility and Financial Backing

Any warranty program is only as reliable as the financial entity backing claims. Contractors should verify A-rated insurance carriers and documented claims payment history.

AM Best's Financial Strength Rating assigns "A" (Excellent) to insurers with excellent ability to meet ongoing obligations, and "A+/A++" (Superior) to those with superior ability. Ratings below "A-" indicate increased vulnerability to adverse conditions.

Verify the specific carrier rating, not just a provider's claim of being "backed by" a rated insurer. Providers like JB Warranties state they are backed by an A+ underwriter; Trinity Warranty lists four A-rated carriers. The reinsurer's track record in the home service space (not just general insurance) reduces compliance risk and improves program design.

Scalability and Recurring Revenue Potential

A well-structured warranty program should function as a recurring revenue engine, turning each installation into a long-term income stream.

AHRI data shows approximately 9.7 million combined central AC and heat pump units shipped in the U.S. in 2024. Each installation represents a potential warranty sale. The global HVAC services market is projected to reach $97.9 billion by 2030, growing at 6.2% annually.

Programs allowing contractors to invest premium funds for additional ROI, or to grow their own warranty company as the customer base scales, offer compounding financial advantages. Third-party arrangements cap your upside at the commission rate; reinsurance models scale profit proportionally with volume.

How WarrantyRE Can Help HVAC Businesses Own and Manage Their Warranty Programs

WarrantyRE is a reinsurance partner with over 30 years of experience helping home service contractors establish and manage their own administrator obligor reinsurance companies.

Founded in 1994 in Southeast Virginia, the company eliminates the need for third-party warranty providers by enabling contractors to own their warranty structure entirely.

Core Offering

WarrantyRE helps HVAC contractors set up their own warranty company, backed by A-rated insurers, so contractors capture 100% of warranty profits their customer base generates.

Warranty fees are built directly into job pricing, deposited into a legally owned reinsurance account, and used to cover claims—with unused funds remaining as contractor profit.

Key Advantages

This ownership model delivers several practical benefits for HVAC contractors looking to control their warranty operations:

WarrantyRE evaluates your revenue, job volume, current warranty practices, tax liabilities, and callback costs to determine program viability and profitability potential. The company handles all legal entity formation, state filings, and compliance requirements so you can focus on installations.

The program includes complete administrative support:

- Adjudicates claims from first call to final resolution

- Manages compliance for IRS Code 831(b) and state licensing

- Delivers monthly financial statements and performance reporting

- Handles bookkeeping and tax filings

- Processes all legal forms, renewals, and regulatory filings

Standard program fees cover all administration without unexpected charges. Any additional costs (specialized legal advice, optional customizations) are agreed upon upfront.

Tax and investment benefits:

- Contributions to the reinsurance account reduce taxable income

- Premium reserves are placed in conservative government bonds or other vehicles acceptable to insurance regulators

- Once reserves exceed 125% of unearned premiums, excess funds may be invested more aggressively at your direction

- All investment income belongs to your reinsurance company

Unique Value for HVAC Contractors

Each installation becomes recurring revenue, with callbacks cost-controlled through structured reserves. Contractors gain financial and operational control that third-party programs structurally prevent.

The program transforms labor warranties from a liability into a profit center while improving cash flow and customer satisfaction.

Conclusion

Choosing a warranty program for your HVAC business is ultimately about deciding who controls the financial upside of customer relationships.

Contractors who rely entirely on third-party providers fund someone else's profitability—retaining 24-30% while the administrator keeps the rest.

The best warranty program aligns with your long-term growth goals, offers genuine claims control, and creates recurring revenue.

This is not a one-time setup decision. As your business scales, customer volume grows, and better program structures become accessible, revisit your warranty strategy regularly. Ensure you're capturing the value your installations generate—not leaving it on the table for third-party providers to claim.

Frequently Asked Questions

What is the $5000 rule for HVAC?

The $5,000 rule helps homeowners decide between repair and replacement by multiplying the system's age by the repair cost—if it exceeds $5,000, replacement is recommended. HVAC contractors use this rule to structure warranty coverage terms and advise customers, especially when determining labor warranty coverage for older systems.

What is the 20 rule for HVAC?

The "Rule of 20" compares repair cost against system age and replacement value to guide customer decisions. Contractors use this framework to structure warranty programs appropriately for older versus newer systems, ensuring coverage aligns with realistic failure probabilities.

What is the difference between a manufacturer warranty and an extended warranty for HVAC?

A manufacturer warranty covers factory defects (typically 5-10 years for parts), while an extended warranty covers ongoing repairs beyond that window and includes labor costs. Contractors who offer extended warranties control the customer relationship and create recurring revenue that manufacturer warranties don't provide.

Can HVAC contractors offer their own warranty programs to customers?

Yes, contractors can offer their own warranty programs through branded service plans or reinsurance-backed warranty companies. This allows them to retain premium revenue, control claims, and build financial value instead of paying third-party administrators.

How does a reinsurance-backed warranty program work for an HVAC business?

The contractor establishes their own warranty company supported by A-rated insurers, collects premiums from customers, pays claims from that pool, and retains all underwriting profit. The reinsurer provides financial backing and compliance, while the contractor controls claims and captures margins that would otherwise go to third-party administrators.