Introduction

Customers now expect labor warranty coverage as standard, but most contractors lack a structured program to deliver it profitably. Without one, every callback drains margin and disrupts operations rather than building loyalty.

According to a 2023 survey of over 10,000 homeowners, 50% would decline a bid due to lack of warranty—the third most common deal-breaker after poor attitude and lack of professionalism.

A labor warranty program is more than a promise—it's a business system that requires defined scope, a funding model, written documentation, and a claims process to work profitably.

Without these elements, contractors silently absorb callback costs that can reach $650 per incident for HVAC service callbacks and $850 for install-related returns, according to ACCA's analysis of contractor callback costs.

Setting up a structured program requires assessing your current operations, defining coverage terms, building a funding model, and establishing a claims process. Done right, it transforms callbacks from cost centers into revenue opportunities.

You'll learn what to evaluate before launching, how to structure the program for profitability, and which mistakes cause most programs to fail.

TLDR

- Labor warranties cover repair costs for 1–2 years post-installation

- Choose from three models: self-funded, third-party provider, or reinsurance-backed (you own and profit)

- Calculate callback rates and costs upfront to price your program profitably

- Written policy signed at installation is legally required—verbal warranties create disputes and offer no protection

- Proper pricing and structure can transform warranty programs from cost centers into profit centers

What Is a Contractor Labor Warranty Program?

A contractor labor warranty is a formal commitment to return to a job and cover labor costs for qualifying repairs within a specified period after installation.

This is distinct from manufacturer parts warranties. While manufacturers like Carrier, Rheem, or A.O. Smith cover equipment defects, your labor warranty covers the cost of returning to fix installation-related issues.

According to the National Roofing Contractors Association, there is "no industry standard" for contractor workmanship warranties, though many contractors offer one to two years of coverage.

The National Association of Home Builders' Residential Construction Performance Guidelines (6th edition, 2022) explicitly distinguishes between contractor warranties and manufacturer warranties.

What Labor Warranties Cover vs. What They Don't

Covered under labor warranties:

- Technician time and travel for installation-related callbacks

- Diagnostic work for workmanship defects

- Re-installation labor for improper initial installation

- Labor to correct installation errors (leaking pipes, improper wiring, HVAC system failures due to installation issues)

Excluded from labor warranties:

- Manufacturer parts failures (covered by equipment warranty)

- Customer-caused damage or modifications

- Work performed by other contractors after original install

- Normal wear and tear

- Pre-existing conditions

- Storm damage or acts of nature

- DIY repairs attempted by homeowner

- Consumable items

Understanding what's covered clarifies the scope of your obligation. The next question is how to fund it.

The Three Program Structures

Contractors fund labor warranty programs through three primary models:

1. Self-Funded (Contractor-Funded) You absorb all callback costs directly from operating cash. This works for low-volume operations with predictable claims.

The risk: cash flow exposure to unpredictable spikes. No external fees, but no financial protection.

2. Third-Party Provider You pay a per-install fee to an external warranty company that assumes claim responsibility.

This transfers risk but also transfers underwriting profit to the provider. You gain predictability but lose control over claims decisions and financial upside.

3. Reinsurance-Backed You establish your own warranty entity, collect premiums from customers, and capture underwriting profit when claims run below premiums.

An A-rated insurer provides a financial backstop for catastrophic scenarios. This is the only model where you own the financial upside.

Companies like WarrantyRE help contractors structure and fully administer reinsurance-backed programs, handling entity formation, claims processing, compliance management, and financials while you retain ownership and profit potential.

What to Assess Before Setting Up Your Program

Skipping pre-setup analysis is the most common reason warranty programs lose money. Outcomes depend heavily on historical performance data and regulatory requirements specific to your state.

Claims Exposure Baseline

Calculate these three metrics before building your program:

1. Historical Callback Rate Express callbacks as a percentage of total installs. ACCA research shows that a 5% callback rate is "more common than we'd all like to admit" for mid-sized HVAC contractors, while ACCA's Quality Installation certification targets 2%. FieldEdge benchmarks place acceptable HVAC callback rates at 2%–2.75%.

2. Average Labor Cost Per Callback Include technician time, travel, overhead, and lost opportunity cost. ACCA's model shows:

- Service callback: approximately $650 ($100 tech labor + $300 overhead + $250 lost revenue)

- Install callback: approximately $850 (3 hours total)

3. Service Lines Generating Most Callbacks Track which installations generate higher warranty claims. For example, HVAC contractors may see higher callbacks on refrigerant-related work, while plumbers may experience more callbacks on fitting installations.

These three numbers drive both funding model selection and pricing structure.

State Compliance Requirements

Labor warranties and extended service agreements fall under insurance or service contract law in many states, with requirements varying significantly.

Florida Requirements:

Florida Statute Chapter 634 requires service warranty associations to:

- Obtain licensing as a service warranty association

- Maintain minimum net assets of $300,000

- Hold 25% unearned premium reserve

- Post $100,000 statutory deposit

- Maintain maximum 10:1 premium-to-asset ratio

- Deliver each contract within 45 days of purchase

Reimbursement insurance covering 100% of claims exposure can offset the 25% reserve requirement.

New York Takes a Different Approach:

New York Insurance Law Article 79 requires:

- Registration with Department of Financial Services ($250 every 2 years)

- Financial security via one of three pathways:

- 100% reimbursement insurance from authorized NY insurer

- 40% funded reserve plus 5% financial security deposit (minimum $25,000)

- $100 million net worth

- Important exemption: "Express or implied warranties" are exempt—a standard workmanship warranty included with a job may not trigger registration

These two states illustrate how varied compliance requirements can be. Over 40 states have some form of service contract regulation, according to NAIC tracking.

Consult a compliance attorney before launching your program.

Structural Fit by Business Volume

Match your program structure to your business scale:

Self-Funded Programs: Work best for contractors with annual revenue under $500K, where claims are infrequent and predictable. Risk exposure is manageable, and administrative overhead is minimal.

Third-Party Providers: Offer simplicity for mid-volume businesses ($500K–$2M annual revenue). These contractors generate enough volume to justify the per-install fee but lack the scale to justify building their own reinsurance infrastructure.

Reinsurance-Backed Programs: Offer the strongest profit potential for contractors doing significant install volume. While specific thresholds vary, contractors generating $1M+ in annual install revenue typically see meaningful profit capture from the reinsurance model. The administrative requirements (entity formation, claims management, compliance) are handled by administrators like WarrantyRE, making this model accessible even for mid-sized contractors.

This revenue-based framework matters because industry data shows most HVAC companies fall in the $500K–$2.5M range, with net profit margins between 8%–12%. For businesses in this sweet spot, capturing warranty underwriting profit can materially impact bottom-line performance.

How to Set Up a Labor Warranty Program

Step 1 — Define the Scope of Your Coverage

Determine exactly which services, equipment types, and failure scenarios qualify:

Covered Services:

- Installation defects and workmanship errors

- Labor to diagnose and repair installation-related failures

- Return visits within the warranty period for qualifying issues

Explicit Exclusions:

- Pre-existing conditions discovered during service

- Customer modifications or DIY repairs after installation

- Work performed by other contractors

- Manufacturer equipment failures (covered separately)

- Consumables (filters, batteries, etc.)

- Storm damage, flooding, or acts of nature

- Failure to maintain equipment per manufacturer specifications

Operational Parameters:

- Geographic service area limits

- Response time commitments (e.g., 48 hours for non-emergency callbacks)

- After-hours callback terms and fees

- Service call fees, if applicable

Draft a complete exclusions list at this stage. Ambiguity in scope is the root cause of most warranty disputes.

Step 2 — Choose and Set Up Your Funding Model

Evaluate the three funding options based on your claims exposure data:

Self-Funded Model:

- Simple to implement—no external contracts

- Exposes cash flow to unpredictable claims spikes

- No administrative fees but no financial protection

- Works best for low-volume contractors with predictable claim patterns

Third-Party Provider Model:

- Transfers risk to external warranty company

- Predictable per-install cost structure

- Contractor pays for simplicity but loses underwriting profit

- Provider controls claims decisions and customer experience

- Ideal for mid-volume contractors prioritizing simplicity over profit capture

Reinsurance-Backed Model:

- Contractor owns the warranty program and captures underwriting profit

- Warranty fees collected from customers fund the program

- A-rated insurer provides financial backstop for catastrophic scenarios

- Requires entity formation, claims review, compliance management, and financial administration

For contractors who want to capture warranty profits but lack internal resources, specialized administrators like WarrantyRE handle entity formation, claims processing, compliance monitoring, and financial reporting. This makes the reinsurance model accessible even for mid-sized contractors.

Reinsurance-backed programs suit contractors seeking to maximize profitability and control over warranty operations.

Step 3 — Write the Warranty Policy Document

Your written policy must include the following elements:

Required Elements:

- Contractor business name, license number, and contact information

- Customer name and installation address

- Installation date and detailed job description

- Warranty term: start date, end date, coverage period (e.g., "1 year from installation date")

- Covered services and equipment listed specifically

- Complete exclusions list from Step 1

- Service call fees for callback visits, if applicable

- Claims filing instructions (how to request service, required documentation)

- Voiding conditions (non-payment, customer modifications, failure to maintain)

A signed written policy at installation protects the contractor as much as the customer—without documentation, verbal promises become costly disputes that are nearly impossible to enforce.

Have your policy reviewed by a state-licensed attorney before rollout, particularly to confirm any state-required service contract language.

Step 4 — Price the Warranty Into Your Services

Calculate expected cost per install:

Formula: Expected Cost = (Callback Rate × Average Callback Cost) × Buffer Margin

Example Calculation:

- Callback rate: 3% (0.03)

- Average callback cost: $650

- Expected cost per install: 0.03 × $650 = $19.50

- Add 50% buffer margin: $19.50 × 1.50 = $29.25

- Warranty price per install: $30–$35

The buffer margin (40%–50%) protects against high-claim periods. Call volumes spike during peak seasons. Samsara's analysis of 65 million HVAC service trips shows summer months bring 20%–40% higher service demand, creating proportionally greater callback exposure.

Two Pricing Approaches:

Bundled Pricing: Include warranty in base install price, present as value-add. Example: "$8,500 installation includes 2-year labor warranty."

Tiered Pricing: Offer choice between basic and premium coverage. Example:

- Standard install with 1-year warranty: $8,500

- Premium install with 3-year warranty: $8,950

Tiered pricing increases average ticket and makes warranty feel like a customer choice rather than a fee.

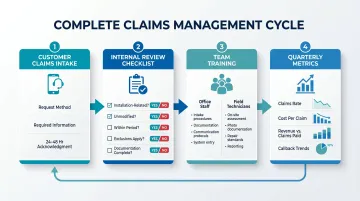

Step 5 — Build Your Claims Process and Train Your Team

Customer Claims Process:

- How customers request service (phone, email, portal)

- Required information (installation date, description of issue, contact details)

- Response time commitments (24–48 hours for acknowledgment)

- Service appointment scheduling

Internal Review Checklist:

- Was the failure installation-related or equipment-related?

- Is the equipment in original, unmodified condition?

- Is the claim within the warranty period?

- Do any exclusions apply?

- Is documentation complete?

A written checklist prevents inconsistent field decisions. Without it, profitability erodes and customer trust suffers.

Training Requirements:

Office Staff:

- Explaining warranty at point of sale

- Registering warranties in system

- Routing inbound claims

- Documenting review decisions

Field Technicians:

- Using the review checklist

- Completing callback documentation

- Communicating warranty decisions professionally

- Identifying patterns in callback causes

Quarterly Performance Metrics:

- Claims rate per install category

- Average cost per claim

- Total warranty revenue vs. claims paid

- Callback trends by service line or technician

Key Parameters That Determine Program Success

Program outcomes depend on controlling four core variables. Most programs that fail do so because one of these is ignored or underestimated.

Coverage Term Length

Longer terms increase exposure but allow higher warranty fees and stronger competitive positioning.

Standard Coverage Terms by Trade:

- HVAC: 1-year baseline, 2–3 years competitive, 5–10 years premium

- Roofing: 1–2 years baseline (NRCA notes "no industry standard"), 5 years competitive, 10+ years premium

- Plumbing: 1-year baseline, 3–10 years via third-party or reinsurance

- Electrical: 1-year baseline

Match coverage duration to your claims history and pricing buffer. A 5-year term without financial modeling is an unquantified liability.

Extended terms work best in reinsurance-backed models where reserves accumulate over time and investment income offsets long-tail exposure. This structure allows contractors to offer competitive coverage while managing risk through proper reserve allocation.

Exclusion Clarity and Enforcement Consistency

Vague exclusions generate disputes. Inconsistent enforcement erodes both profitability and customer trust.

Consider this scenario: One technician approves a callback for a customer-modified system "to maintain goodwill," while another denies an identical claim citing policy exclusions.

The customer whose claim was denied feels cheated, and you've now set a precedent that undermines your written policy. The claims review checklist from Step 5 prevents this problem—every technician applies the same criteria to every claim, with documentation explaining the decision.

Pricing Buffer Adequacy

Insufficient pricing buffer is the most common reason self-funded and underprepared programs lose money.

ACCA data shows that reducing callback rates from 5% to 2% saves approximately $50,000 annually for a $2M revenue contractor.

But even well-run programs experience seasonal spikes—HVAC call volume can reach 3–5× base levels during summer, creating proportionally higher callback exposure.

Your pricing buffer must account for:

- Seasonal claim spikes

- High-risk install categories

- Technician variability

- Economic conditions affecting claim frequency

A 40%–50% buffer above expected cost provides reasonable protection for most contractors.

Claims Documentation and Recordkeeping

Every claim—paid or denied—should be documented in writing with the claims review decision and supporting reason.

This data feeds quarterly performance reviews that allow you to:

- Identify which service lines generate disproportionate claims

- Spot training gaps or installation quality issues

- Evaluate whether pricing models are holding up over time

- Adjust coverage terms or exclusions based on actual experience

Rising claims in a specific install category often signal a training or installation quality problem, not a pricing problem. Catching it early prevents compounding losses.

Common Mistakes Contractors Make When Setting Up a Labor Warranty

Offering Warranties Verbally or Informally

This is equivalent to writing a blank check. Verbal warranties are the hardest to enforce and the easiest to dispute.

Customers remember what they want to remember. Contractors have no written record to reference when disputes arise.

Failing to Price the Warranty Separately

Treating warranty coverage as a "free perk" means the business silently absorbs callback costs from operating margin. Over time, this eats away at profits in ways that aren't visible until claims volume spikes.

At a 5% callback rate and $650 per callback, a contractor completing 200 installs annually absorbs $6,500 in unrecovered warranty costs.

Skipping State Compliance Review Before Launching

Many states regulate extended service agreements as insurance products. Contractors who launch without understanding their state's requirements risk operating out of compliance.

This can result in cease-and-desist orders, penalties, or registration suspension. It's especially important for contractors considering the reinsurance-backed model, as entity formation and reserve requirements vary by state.

Ignoring Claims Data After Launch

Reviewing your program quarterly isn't optional. Rising claims in a specific install category often signals a training or installation quality problem, not a pricing problem.

For example, if HVAC refrigerant-related callbacks spike, the issue may be technician certification gaps, not inadequate warranty pricing. Catching patterns early prevents compounding losses and allows targeted training interventions.

Frequently Asked Questions

What is a labor warranty?

A labor warranty is a contractor's commitment to perform qualifying repairs at no additional labor cost within a defined period. It covers workmanship defects, not parts failures or customer-caused damage.

What is a typical contractor warranty?

Most contractors offer a 1-year labor warranty as baseline, with competitive contractors offering 2-year coverage and premium programs extending to 5–10 years. Specific terms, exclusions, and coverage vary by contractor and should always be documented in writing.

Are labor warranties worth it?

Yes—a properly structured warranty program reduces sales objections, supports higher pricing, and when reinsurance-backed, generates profit instead of draining margin. The key is building it as a funded system, not absorbing callbacks informally.

How to create a warranty policy?

Create a written document specifying coverage term, covered services, exclusions, claims process, and voiding conditions. Customers should sign it at installation, and an attorney should review it before use.

What documents are needed for a warranty claim?

Customers need the installation date, original contract, and issue description. Contractors handling claims internally need the adjudication checklist, technician findings, and documented coverage decision.

Do I need to register to get warranty?

Registration requirements depend on the state. Some states require contractors offering extended service agreements or labor warranties to register with a regulatory body, carry reimbursement insurance, or meet financial reserve requirements. Contractors should confirm their state's specific service contract laws before launching a program.

Setting up a labor warranty program requires upfront analysis and disciplined execution, but contractors who structure programs correctly turn warranty exposure into competitive advantage—capturing profits while building customer loyalty.