This guide covers everything you need to know: what warranty labor rates are, how submission options differ, the CPI trap, and actionable steps to claim the maximum rate you're entitled to under state law.

TLDR:

- Statutory submissions typically outperform factory submissions by 15% or more in labor rate increases

- CPI programs lock you into 2-3% annual increases while blocking higher statutory submissions for up to 3 years

- Most states allow one submission per year—missing your window costs 12 months of potential revenue

- Proper statutory submissions can add hundreds of thousands in annual gross profit

- Owning your reinsurance company captures warranty profits third-party providers currently keep

What Is a Warranty Labor Rate (and Why Does It Matter)?

A warranty labor rate is the per-hour reimbursement a manufacturer or warranty provider pays a dealer or service business for labor performed on vehicles covered under warranty. This differs from what customers pay out of pocket for non-warranty repairs.

Why the Rate Matters Financially

The gap between your warranty rate and customer-pay rate directly impacts your bottom line.

A dealership averaging 500 warranty hours per month loses approximately $222,000 in annual gross profit when the gap between a retail labor rate of $197 and an OEM-approved rate of $160 exists—a $37/hour difference.

Industry Benchmarks

- Warranty work accounts for 25% to 50% of a dealership's service revenue when managed effectively

- NADA Data shows dealership service labor warranty revenue reached $6.32 billion in H1 2024, up from $5.33 billion in H1 2023

- The total U.S. automotive warranty market reached $28 billion in 2024, a 19.9% surge from $23.5 billion in 2023

Proper statutory submissions can yield a 15% higher labor rate, 16% higher parts rate, and an 18% jump in warranty gross profit compared to accepting manufacturer-set rates.

Your Legal Right to Fair Compensation

These financial impacts aren't something you have to accept passively. All fifty U.S. states now have laws in their dealer franchise statutes requiring manufacturers to reimburse dealers at reasonable rates—generally no less than what the dealer charges retail customers for the same work.

This legal framework gives you a solid basis to request higher rates.

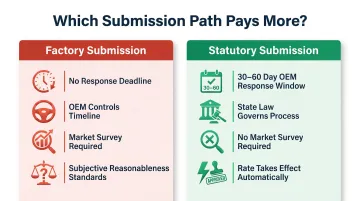

Factory vs. Statutory Submissions: Which Path Pays More?

Understanding the difference between factory and statutory submissions is the single most important decision in the warranty rate increase process. The path you choose determines your timeline, your leverage, and ultimately how much money you recover.

Manufacturer (Factory) Submissions

Factory submissions follow the manufacturer's own policies. You compile qualifying repair orders, calculate an average labor rate, and submit to the OEM following their internal procedures. This path comes with significant disadvantages:

- Manufacturers control the timeline with no obligation to respond within a set period

- OEMs have significant freedom to push back, request market surveys, or reduce your proposed rate

- The process is designed to limit rate increases, not maximize your reimbursement

- Manufacturers can impose subjective standards like "reasonableness" comparisons to market peers

Statutory Submissions

State law governs statutory submissions, not manufacturer policy. This shifts the power dynamic significantly in your favor.

Statutory submissions offer critical advantages:

- Manufacturers must respond (approve or dispute) within a defined window—typically 30 to 60 days

- No market survey required in most states

- Your declared rate goes into effect after the statutory period unless the OEM can prove "material inaccuracy"

- Legislative trends continue strengthening dealer protections

Recent State-Level Protections

2024-2025 legislative updates across multiple states have narrowed manufacturer defenses:

- California limits OEMs to 30 days to contest the "material accuracy" of submissions

- New York shifted the benchmark from OEM time studies to third-party retail labor-time guides

- Illinois prohibits OEMs from recovering costs through chargebacks or "cost recovery fees" to offset higher reimbursement rates

- Virginia, Alaska, New Jersey, and Wyoming established statutory floors and limited manufacturer audit powers

When Factory Submissions Make Sense

Factory submissions may be appropriate if the OEM's sample size requirement is smaller than your state statute requires, potentially yielding faster results. However, the right choice depends on your specific situation and state law. Most dealers find statutory submissions deliver significantly higher rates.

The Hidden Trap of CPI-Based Programs

CPI (Consumer Price Index) programs automatically increase your warranty labor rate each year based on inflation indexes. Manufacturers pitch them as convenient, hands-off solutions that require no annual submission work.

The Problem with Convenience

CPI-based programs historically yield only 2-3% increases annually—a modest adjustment that rarely keeps pace with the real-world cost of parts, labor, and overhead.

That modest increase comes with a catch. Once enrolled, dealers are often locked out of submitting a statutory or factory rate increase for the duration of the program—sometimes up to 3 years.

You're effectively waiving your right to a data-driven, market-rate submission.

The Real Cost

Statutory submissions "consistently outperform CPI programs" because they're based on actual customer-pay averages, not manufacturer-set formulas. The difference is substantial:

- Statutory submissions reflect real market rates from your customer-pay data

- Dealers see increases that translate into "tens—or often hundreds—of thousands of dollars in additional annual gross profit"

- A three-year CPI enrollment can mean forfeiting tens of thousands in recoverable profit

One case study showed a 15-rooftop dealership group saved $4.5 million by switching from manufacturer-set rates to state-statute rates.

Bottom line: Convenience is not worth the long-term revenue sacrifice.

How to Maximize Your Warranty Labor Rate Increase: Step-by-Step

Step 1 — Know Your State's Law

Research your state's warranty reimbursement statute before you begin. Key information to confirm:

- Does your state have a warranty reimbursement statute?

- How many qualifying repair orders must you submit?

- What is the eligible timeframe for repair orders?

- What are the OEM response deadlines?

- How frequently can you submit?

Most states allow one submission per calendar year, and laws have been evolving rapidly as of 2024-2025. Missing details can undermine your entire submission.

Step 2 — Pull the Right Repair Orders

Your submission's quality hinges on selecting the right repair orders. Only qualifying customer-pay (non-warranty) repair orders count, and many categories are automatically excluded under most state statutes.

Exclude these categories (most statutes disqualify them):

- Tires and tire-related services

- Batteries

- Routine maintenance (oil changes, fluids, filters)

- Glass work

- Body work

- Accessories and aftermarket installations

- Vehicle reconditioning

- Wholesale or fleet sales

- Internal/dealership-owned vehicle work

- Goodwill or policy adjustments

- Discounted or promotional work

Strategic order selection—not just pulling sequential records—can significantly affect your calculated average rate. Including excluded repair types skews your rate downward and gives manufacturers grounds to dispute the submission.

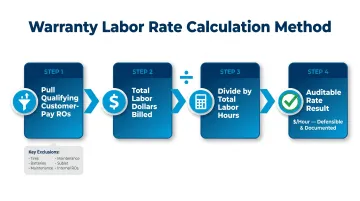

Step 3 — Calculate Your Effective Customer-Pay Labor Rate Accurately

Divide total labor dollars billed on qualifying repair orders by total labor hours worked on those same orders. The calculation must be precise and auditable.

Example calculation method:

- Indiana statute requires 100 customer-paid sequential repair orders or 90 consecutive days of customer-paid repair orders

- Minnesota uses similar approach: total customer labor charges divided by total labor hours

Even small errors in this calculation can undermine your submission or give the manufacturer grounds to dispute it. Ensure your calculation method is clean and auditable.

Step 4 — Submit on Time and Completely

Dealers most often miss their entitled rate by submitting late or incomplete packages. Timing and completeness are non-negotiable.

Critical requirements:

- Know your submission window and calendar deadlines

- Include all required documentation (repair orders, calculation sheets, supporting records)

- Verify the package is complete before sending

- Track delivery confirmation—some state laws start the manufacturer's response clock the moment they receive the submission

Step 5 — Be Ready to Respond to Pushback

Manufacturers may reject or partially approve your submission, so know in advance what constitutes valid dispute grounds under your state's law versus invalid objections.

Valid dispute grounds (in most amended 2025 statutes):

- Material inaccuracy in the submission data

- Inclusion of excluded repair categories

- Calculation errors

Invalid objections:

- Subjective "unreasonableness" claims

- Market comparisons to other dealers

- Cost recovery concerns

Have a process for resubmitting with corrected documentation within the allowed window if necessary.

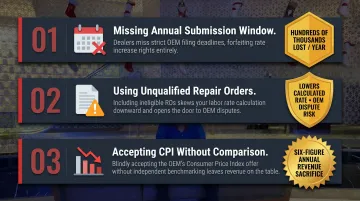

Common Mistakes That Cost Dealers Money

Mistake 1 — Missing the Annual Submission Window

Because dealers can typically only submit once per calendar year, missing the window means waiting another full year—and losing 12 months of potential rate increase revenue.

Mark the submission date on your calendar and treat it with the same urgency as a financial close.

The cost of missing this deadline is significant. One dealer group discovered that missing annual submissions cost them 'many hundreds of thousands of dollars' in profit.

Mistake 2 — Using Unqualified or Poorly Selected Repair Orders

Including excluded repair types (tires, wholesale, routine maintenance) in the calculation lowers your rate and gives manufacturers grounds to dispute the submission.

Common data quality issues include:

- Op codes applied inconsistently by service advisors

- Errors in qualifying repair order selection

- Failure to identify the highest-yielding sequential ROs (the 100 consecutive customer-pay repairs that produce the best rate)

Mistake 3 — Accepting a CPI Program Without Running the Numbers

Dealers who agree to automatic CPI programs without comparing the expected outcome to a statutory submission are often accepting a fraction of what they could earn. This decision should never be made without doing the math first.

Dealers frequently choose the "easier" manufacturer method rather than the more labor-intensive but more profitable state-mandated submission method—a choice that can cost six figures annually.

Beyond Rate Increases: Owning Your Warranty Program

Negotiating better labor rates helps, but you're still working within someone else's system.

Maximizing the labor rate increase you receive from an OEM or third-party warranty provider leaves you dependent on their program, their claims processing, and their profit margins.

The Reinsurance Alternative

Dealers and contractors who establish their own reinsurance company effectively flip the model. Instead of being reimbursed at a capped rate, they capture the warranty premiums and manage the risk themselves.

When you own your reinsurance company, warranty profits—which third-party providers currently retain—flow back to your business. This includes not just labor reimbursement but the full premium pool.

According to AutoNews, in a standard vehicle service contract (VSC) sale of $3,000:

- Dealer keeps $1,500 as front-end retail markup

- Administrator retains $150-$200 as administrative fee

- Remaining $1,300-$1,350 placed into loss reserves

- If only $500 paid in claims, dealer keeps $800 as underwriting profit

- Additional investment income earned on reserve float

Total profit potential per deal: $2,300+ (front-end markup + underwriting gain + investment income).

How the Administrator-Obligor Model Works

In the administrator-obligor reinsurance structure:

- You establish a separate legal entity that acts as your reinsurance company

- Customer warranty fees are deposited into your reinsurance account

- Your reinsurance company pays claims, giving you full control over the process

- Any funds not paid in claims remain with your company

- A-rated insurers back your reinsurance structure, ensuring claims security and regulatory compliance

WarrantyRE: Reinsurance for Dealers and Contractors

WarrantyRE helps dealers and home service contractors set up administrator-obligor reinsurance structures backed by A-rated insurers. The company provides full-service administration including:

- Claims processing from first customer call to final resolution

- Compliance filings and IRS Code 831(b) tax return preparation

- Financial reporting and performance analysis

- Legal forms, filings, and renewals

- Staff training and onboarding

WarrantyRE has helped over 400 automotive dealers establish reinsurance companies, enabling them to offer reinsured warranties, service contracts, GAP, and collateral protection products. The same model applies to home service contractors (HVAC, roofing, plumbing, electrical), allowing them to reinsure labor warranties and turn warranty liabilities into customer-funded revenue streams.

This approach transforms warranty work from a cost center into a controlled, profitable part of your business—the difference between optimizing within someone else's system versus building your own.

Frequently Asked Questions

What is a warranty labor rate?

A warranty labor rate is the hourly amount a manufacturer or warranty provider reimburses a dealer or service business for warranty labor. This rate is typically lower than what the business charges retail customers for non-warranty work.

What is a warranty labor rate increase process?

Dealers compile qualifying customer-pay repair orders, calculate an average labor rate, and submit that data to the manufacturer through either factory submission or statutory submission under state law to establish a higher reimbursement rate.

Do you have to pay for labor if something is under warranty?

In most cases, if a repair is covered under a manufacturer's written warranty, the customer does not pay for labor—the manufacturer reimburses the dealer or service business directly. This is why the warranty labor rate matters so much to the business performing the repair.

Should labor be covered under warranty?

Yes. Under most manufacturer warranties and state laws, labor must be covered for qualifying repairs. Dealers and service providers are entitled to compensation equal to their retail customer rates.

Should dealers own their warranty programs instead of using third-party providers?

Owning your warranty program through reinsurance allows you to capture profits that third-party providers keep. WarrantyRE helps dealers and contractors establish their own reinsurance companies to control their warranty programs and maximize profitability.